- Microstrategy holds 597,000 BTC valued at $64.4 billion, but new accounting rules may trigger taxes on unrealized gains.

- The company faces $350 million in annual debt and dividend obligations, straining cash flow and increasing financial pressure.

- If external financing fails, MicroStrategy may need to sell Bitcoin, potentially impacting market liquidity and its long-term strategy

Microstrategy (NASDAQ: MSTR), the largest corporate holder of Bitcoin, may soon face rising financial pressures despite recording over $20 billion in unrealized gains on its Bitcoin portfolio. New disclosures filed with the SEC in July 2025 reveal several risks tied to recent regulatory changes and the company’s financial structure.

MicroStrategy (MSTR) now holds over 597,000 BTC worth $64.4 billion as of June 30, 2025. This bold approach has placed the firm at the center of attention due to newly reported financial vulnerabilities.

New Accounting Rules May Bring Unexpected Tax Costs

The company’s latest SEC filing, Form 8-K, submitted in July 2025, outlined possible future tax liabilities. These concerns stem from new U.S. accounting rules — specifically ASU 2023-08. The rule requires firms to report bitcoin holdings at fair value, not just when sold.

This change may expose Strategy to a minimum 15% corporate tax under the Corporate Alternative Minimum Tax (CAMT) set to begin in 2026. Since the firm has not liquidated its BTC holdings, taxes may still apply based on unrealized gains. Strategy acknowledged that this rule could create obligations to pay taxes in cash on bitcoin it hasn’t sold.

BTC May Be Sold to Meet Tax or Cash Demands

Despite the popular belief that Strategy never sells its bitcoin, the company may have no choice. The SEC filing clearly warns:

“We may need to liquidate some of our bitcoin holdings or issue additional debt or equity securities to raise cash sufficient to satisfy our tax obligations.”

This means that if the tax burden materializes and alternative funding is unavailable, BTC sales could be triggered. Although the firm previously sold a small amount of bitcoin in Q4 2022, the latest disclosures indicate this option remains on the table.

Core Business Not Covering Financial Burden

Strategy has also admitted that its software operations are not generating enough cash to manage certain financial demands. Specifically, it said:

“We do not expect the cash generated by our software operations to be sufficient to cover such expenses.”

This admission suggests the company will need to rely on its BTC holdings or raise capital to manage its obligations. The reliance on external sources for liquidity introduces a risk if markets tighten or investors pull back.

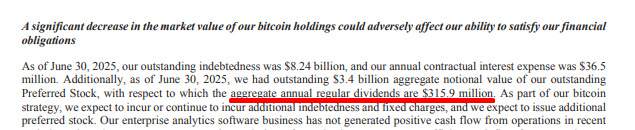

Debt and Dividend Commitments Top $350 Million Annually

As of mid-2025, Strategy holds $8.2 billion in convertible debt and $3.4 billion in preferred stock. These financial instruments come with a steep cost:

- Annual interest on debt totals $36.5 million.

- Preferred stock dividends add $315.9 million yearly.

That brings fixed annual obligations to more than $350 million, regardless of bitcoin’s market value. The preferred stock includes multiple instruments:

- STRK (8% rate)—Paid in cash or limited shares

- STRF (10%)—Cash-only, compounding if unpaid

- STRD (10%)—Requires cash payouts but is non-cumulative

Missed payments could lead to shareholder penalties, dilution of shares, or increased governance involvement, including board seats.

Financing Risks Could Prompt BTC Liquidation

The filing directly acknowledges that if Strategy cannot access new equity or debt markets, it may be forced to sell bitcoin. The statement reads:

“If we are unable to secure equity or debt financing… we may be required to sell bitcoin.”

This contingency is vital because financing options depend on market conditions. If interest rates climb or investor appetite wanes, raising capital may be difficult. In that case, selling BTC could be the only option left. Such moves could affect both the company’s balance sheet and the broader market.

Custodial Risks and Exposure to Market Volatility

Another issue raised relates to how bitcoin is held. Strategy’s filing warns that:

“If our custodially-held bitcoin were… considered to be the property of our custodians’ estates… we could be treated as a general unsecured creditor…”

This means that in the event a custodian fails or enters bankruptcy, the firm may lose access to its BTC. While considered unlikely, the risk is not zero, and such a scenario could create liquidity stress.

Beyond custody, Strategy is highly sensitive to broader macroeconomic factors. The company admits exposure to:

- Bitcoin price fluctuations

- Interest rate movements

- Regulatory policy changes

- Overall liquidity in financial markets

Each of these variables can affect both the firm’s valuation and its access to funding. Given the scale of BTC holdings relative to its operating revenue, this sensitivity is amplified.

A High-Stakes Position Built on Bitcoin

Strategy has positioned itself as a pioneer in corporate BTC investment, achieving sizable unrealized gains. However, according to its own statements, the financial structure supporting this position is exposed to various risks.

With rising regulatory pressure, possible new taxes, heavy debt obligations, and limited operating cash flow, the firm’s bitcoin-centered model faces ongoing challenges. The possibility of BTC sales, previously considered unlikely, now appears listed among several potential responses in the company’s official disclosures.

The situation remains fluid, and Strategy’s next steps will likely be influenced by external market shifts and how the company navigates its growing financial strain.